Special topics

One of the key bodies mandated to ensure proper management of the Ghana Petroleum Funds (GPFs), the Investment Advisory Committee (IAC) has not met since 2016 raising questions about its relevance and impact on the management of the country’s oil revenue. The absence of such an important Committee appears to be giving credence to the suggestion that it is just another bureaucracy with little or no impact on the actual management of the resource revenue.

Ghana discovered oil in 2007, followed by a synthesis of optimism, cynicism and heated public discourse across the country on the management of this finite extractive resource. In the face of these realities, calls by Civil Society Organisations, Independent Policy Research Think Tanks and Development Partners in Ghana for prudent management and investment of revenues from petroleum culminated in the crafting of the Petroleum Revenue Management Act (PRMA) 2011 (Act 815), as amended (Act 893). It is section 29 of this Act that sets up the Investment Advisory Committee (IAC).

The Committee primarily was set up to advise the Finance Minister and for the general performance monitoring of the management of the GPFs which comprises the Ghana Stabilisation Fund and the Ghana Heritage Fund. Ghana is not the only country with such a structure. A variety of advisory committees exist. The Financial Committee of Chile made up of about six members plays a similar role as the IAC of Ghana – providing advice to the Ministry of Finance – on fundamental aspects of the investment policy for the Sovereign Wealth Funds. Uganda’s Public Finance Management Act (2015) also establishes an Investment Advisory Committee to advise the Minister on the investments made under the Petroleum Revenue Investment Reserve. Similarly, the Committee is made up of seven members albeit with a mix of institutional and non-institutional representation. The Investment Advisory Council (IAC) of the United States has a broader advisory role and composed of not more than 20 members established to solicit private sector advice to the Secretary of Commerce on the promotion and retention of Foreign Direct Investment (FDI) to the United States.

Composition & Functions of the IAC

Section 31 of the PRMA stipulates that the IAC be composed of seven members including a woman – who must be persons of proven competence in finance, investment, economics, business management, law or similar disciplines. Three key functions of the IAC as prescribed in the law are:

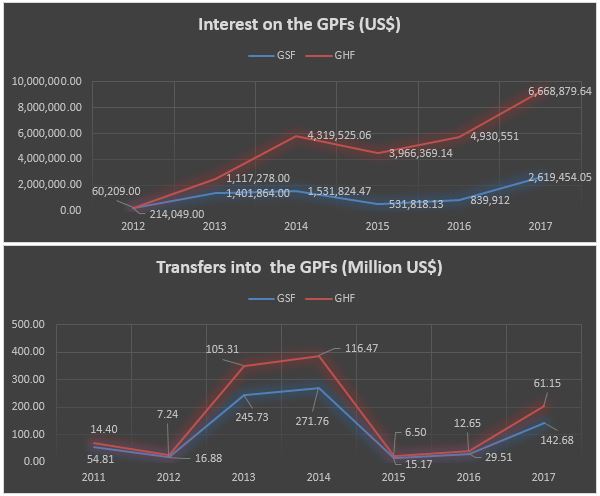

Fig. 1: Transfers into and Returns on GPFs

Sources: Reconciliation Reports on the PHF, PIAC Reports.

A key issue is the mode of appointment of the members of the IAC. Section 31 (4) of the PRMA states that the Minister in consultation with the Governor shall nominate the members of the Investment Advisory Committee for appointment by the President and that the President shall appoint the Chairperson of the Investment Advisory Committee. As the practice has been with such political appointments, what this means is that the IAC unlike PIAC, would be dissolved and reconstituted anytime there’s a change of President. The question is whether this represents best practice. In the case of the Financial Committee of Chile, some members of the Committee have been with the Committee since its inception in 2007. Depoliticisation of the appointment of the Committee cannot therefore be overruled if the Committee is to function properly and achieve the purpose of its establishment.

A valid concern is whether the non-existence of the Committee or the politicisation of appointments onto the Committee serves anyone’s interest. If the Minister in consultation with the Governor nominates the members to be appointed, and given the strategic role of the two nominating authorities in the management of the GPFs, there is a case to be made that the nominations and appointments are laced with intents, wittingly or unwittingly to get people they “can comfortably work with”. Is professionalism sacrificed on the altar of political convenience or is it a case of business as usual?

In accordance with Section 27 of the PRMA, the resources of the GPFs and subsequently the Ghana Petroleum Wealth Fund shall be invested in qualifying instruments prescribed by an Executive Instrument. The range of instruments designated as qualifying instruments shall be reviewed every three years or sooner by the Minister on the advice of the Investment Advisory Committee. Given that the investment instruments are specified, to what extent does the advice of the IAC impact on returns from the GPFs?

The case has also been made that given the fluid nature of the international market and uncertainties clouding the investment climate, the processes prescribed in Act 815 for seeking advice or remedying failure to seek advice from the Committee can potentially affect returns on the GPFs. The waiting period to seek advice from the IAC could actually be money lost.

Conclusions

Based on the lack of any established correlation, a number of arguments can be advanced for or against the existence of the IAC. Given that the Minister can still take decisions in the absence of the advice of the IAC and has indeed been making investment decisions of whatever nature, it can be argued that the Committee may as well be expunged from the law in subsequent reviews and amendments.

Again, considering that the IAC if it were to exist would have incurred costs in its operations (administrative costs and allowances to members), there is a case to be made for prudence, and saving the national kitty of additional public spending pressure. This is particularly so when no clear differences in returns can be seen over the period of non-existence of the Committee as seen from Fig 1.

It is however important to note that if the Committee were to exist and function, where the Minister takes a decision without the advice of the IAC, the Minister shall inform the Committee within forty-eight hours after taking the decision. This apparent violation of the law has persisted over the years. On the flipside, such procedures can be argued to be overly prescriptive and tend to hamper quick decision making in the phase of changing investment circumstances.

In making a case for the existence of the IAC, it cannot be taken for granted that the Committee if it were to exist, may not formulate policy, offer advice, propose guidelines and develop more competitive benchmark portfolios of returns and risks that would change the narrative. Truth is, it cannot be said emphatically that this is the best Ghana could get as a country from the investment of the GPFs.

If the governance issues associated with the appointments and functioning of the IAC are addressed, the Committee can be rightly placed to function and effectively execute its mandate as in the case of other advisory committees on Sovereign Wealth Funds such as that of Chile.